NEW Bima Bachat

LIC's New Bima Bachat:

Ever come across a large pile of banknotes? You know, by winning the lottery or hitting the jackpot at your favorite casino? Your first instinct must have been to buy a Porsche (that can’t really show its true skills owing to the Indian roads and the traffic) or to buy a house that could, possibly, contest for winning the show – MTV Cribs.

But, instead of dwelling on utopia, wouldn’t it be more prudent to consider your immediate surroundings? For example, your mother who loves to have you around just to start a bit of friendly banter or your younger brother who aspires to get into Yale but spends his weekends watching Gossip Girl.

Feeling a little less reckless, aren’t we? The new LIC Bima Bachat Plan is for all those people who would prefer security overspending. It is a single premium participating endowment policy, that is, it is the traditional cash back plan with scheduled payments coupled with the return of the entire premium in addition to loyalty points given at the completion of policy tenure.

LIC's New Bima Bachat is a participating non-linked saving cum protection plan, where the premium is paid in lump sum at the outset of the policy. It is a money-back plan which provides financial protection against death during the policy term with the provision of payment of survival benefits at specified durations during the policy term. In addition, on maturity, the single premium shall be returned along with Loyalty Addition, if any. This plan also takes care of liquidity needs through its loan facility.

1. BENEFITS:

a) Death benefit:

On death during the first five policy years: Sum Assured.

On death after completion of five policy years: Sum Assured along with Loyalty Addition if any.

b)Survival Benefits:

Payable as given below in case of Life Assured surviving to the end of the specified duration:

For policy term 9 years: 15% of the Sum Assured at the end of each of 3rd & 6th policy year

For policy term 12 years: 15% of the Sum Assured at the end of each of 3rd, 6th & 9th policy year

For policy term 15 years: 15% of the Sum Assured at the end of each of 3rd, 6th, 9th & 12th policy year

c) Maturity Benefit:

Payment of Single Premium (excluding taxes and extra premium, if any) along with Loyalty Addition, if any, in case of Life Assured surviving to the end of the policy term.

d) Loyalty Addition:

Depending upon the Corporation's experience the policies shall participate in the profits and shall be eligible for Loyalty Addition. The Loyalty Addition, if any, is payable on death after completion of five policy years and on policyholder surviving to maturity, at such rate, and on such terms as may be declared by the Corporation.

For policy term 9 years: 15% of the Sum Assured at the end of each of 3rd & 6th policy year

For policy term 12 years: 15% of the Sum Assured at the end of each of 3rd, 6th & 9th policy year

For policy term 15 years: 15% of the Sum Assured at the end of each of 3rd, 6th, 9th & 12th policy year

c) Maturity Benefit:

Payment of Single Premium (excluding taxes and extra premium, if any) along with Loyalty Addition, if any, in case of Life Assured surviving to the end of the policy term.

d) Loyalty Addition:

Depending upon the Corporation's experience the policies shall participate in the profits and shall be eligible for Loyalty Addition. The Loyalty Addition, if any, is payable on death after completion of five policy years and on policyholder surviving to maturity, at such rate, and on such terms as may be declared by the Corporation.

About LIC Bima Bachat:

- It is a simple money back plan, wherein an individual buys this by paying a single lump-sum premium to get periodic repayment for various life goals

- The single premium is based upon the fixed policy term of 9 or 12 or 15 years

- A periodic repayment after every 3rd year till maturity

- Bima Bachat plan provides risk cover and loyalty additions on maturity

- It offers rebates on the higher sum assured chosen

Eligibility Criteria:

Eligibility Criteria Minimum Maximum Sum Assured (in Rs.) Rs. 35,000 No Limit Policy Term (in years) 9yrs, 12yrs,15yrs Premium Payment Term (in years) Single Premium Entry Age of Life Insured (in years) 15yrs 66yrs Age at Maturity(in years) - 75yrs Premium (in Rs.) Nothing Specified Payment Modes Yearly, Half-yearly, Quarterly, Monthly and SSS A Few Obligations To Keep In Mind Regarding The LIC New Bima Bachat Plan:

Some rules that all policyholders must abide by:

1. LIC New Bima Bachat policy attains maturity when the investor turns 75 years of age.

2. There are three choices of policy term offered to the investor depending on their age and requirements – 9, 12 and 15 years, among which the applicant must choose at the time of application.

3. The minimum sum assured varies as the term of the policy. For nine years’ term, a minimum of Rs 35000 must be insured, whereas, for 12 years’ and 15 years’ terms, Rs 50000 and Rs 70000 are the minimum amounts of premiums required, respectively.

4. Also, the applicant must keep in mind that the amount assured must be a multiple of Rs 5000.

5. To make things easier, the LIC Bima Bachat Plan requires a single premium only.

Key Details Of The LIC New Bima Bachat Plan:

Want to know what you’re getting into with this insurance policy? After all, not every life insurance plan is synonymous with each other. Take a look at the features that this policy entails:

1. It is a single premium cash back plan, that is, the lump sum of money is invested in the policy in return for a death benefit.

2. The loyalty addition promised is payable upon maturation of policy or on earlier demise.

3. 15% of the sum assured is returned after three years as a survival benefit (will be elaborated later).

4. Discount is provided on the higher sum assured.

5. Surrender Benefit or Policy Termination: Within the first year of the policy term’s commencement, if the applicant withdraws, 70% of the single premium is returned excluding taxes. If one retreats after the 2nd year launches, then 90% of the single premium is returned.

6. If the policy seems unapproachable for you, the option of canceling the LIC New Bima Bachat Plan within 15 days rests with you.

Advantages Of The LIC New Bima Bachat Plan:

What’s so tempting about this policy? Why should you revoke your desire to spend all your money in one go and become a dull person investing in policies? Read on to find out.

Inclusions:

There are a few honorable mentions, when it comes to the prime benefits of the LIC Bima Bachat Plan, making it one of the most sought-after life insurance policies. Loans can be availed against 60% of the surrender value, under this life insurance plan.

Exclusions:

If the policyholder’s death results due to suicide within a year of the policy tenure, only 90% of the sum assured is returned to the nominee.

TAX SAVINGS:

If the annual premium of a life insurance plan exceeds 10% of the Sum Assured, the proceeds from such life insurance plan are not exempt from tax.

Even for the tax benefit for payment of annual premium under Section 80C, you get tax benefit only to the extent of Actual Premium Paid or 10% of Sum Assured, whichever is lower.

There is a minor exception in case of differently-abled persons or those suffering from specified ailments.

Suppose your life insurance plan has an annual premium of Rs 1.25 lacs and the life cover is Rs 8 Lacs. In this case, tax benefit under Section 80C will be capped at Rs 80,000.

Moreover, any proceeds from such life insurance plans are taxable.

Now, there is TDS deducted for such policies. So, there is no way you can fly under the tax radar.

One aspect that I am not sure about is whether you get an adjustment for the premium paid before you calculate tax liability. In my opinion, you shouldn’t. However, I have read about adjustment at many places. A good Chartered Accountant can answer this better

NEW BIMA BACHAT EXAMPLE:

Example – Suppose Abhi of age 35 buys a policy of Rs. 5 lakhs (Sum Assured) for a term of 12 years. He will have to pay a Single Premium of Rs. 3,64,415. It comes to Rs. 3,78,081 after taxes.

Scenario 1 – Abhi survives until the end of the policy term.

Since it is a 12-year policy, he would receive Survival Benefit payments at the end of the 3rd, 6th and 9th policy year as follows:

Scenario 1 – Abhi survives until the end of the policy term.

Since it is a 12-year policy, he would receive Survival Benefit payments at the end of the 3rd, 6th and 9th policy year as follows:

- 3rd policy year – 15% of Sum Assured = 15% of Rs. 5,00,000 = Rs. 75,000

- 6th policy year – 15% of Sum Assured = 15% of Rs. 5,00,000 = Rs. 75,000

- 9th policy year – 15% of Sum Assured = 15% of Rs. 5,00,000 = Rs. 75,000

Also, when the plan matures after 12 years, the Single Premium paid which is Rs. 3,64,415 and Loyalty Additions would be paid to him.

Scenario 2 – Abhi dies after 7 years of buying the plan

In such a scenario, he would have received the following Survival Benefit payments:

Scenario 2 – Abhi dies after 7 years of buying the plan

In such a scenario, he would have received the following Survival Benefit payments:

- 3rd policy year – 15% of Sum Assured = 15% of Rs. 5,00,000 = Rs. 75,000

- 6th policy year – 15% of Sum Assured = 15% of Rs. 5,00,000 = Rs. 75,000

Additionally, the Sum Assured of Rs. 5 lakhs would be paid irrespective of any money-back benefits already received. The Loyalty Additions accumulated would also be paid as the policy has completed 5 years.

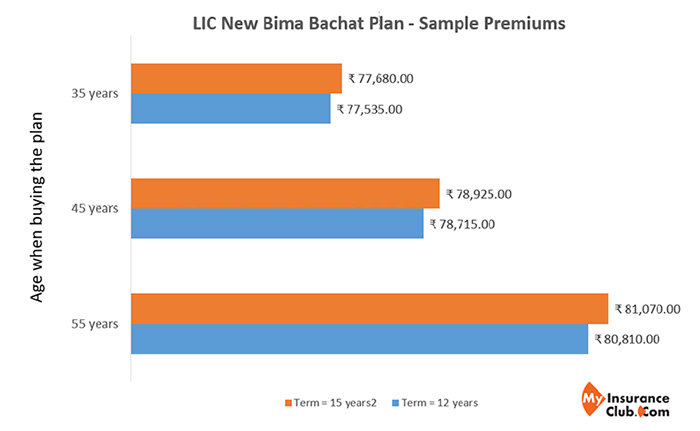

Sample Premium Rates for LIC Bima Bachat Policy:

The below illustration is for a healthy Male (non-tobacco user) opting for a

Age = 35 years, 45 years and 55 years

Sum Assured = Rs 1,00,000

Policy Term = 12 and 15 years

Age = 35 years, 45 years and 55 years

Sum Assured = Rs 1,00,000

Policy Term = 12 and 15 years

CHECK HERE ABOUT YOUR PREMIUM AND MATURITY AMOUNT:

VIDEO TUTORIAL:

No comments:

Post a Comment